Elevate Financial Planning turns 1! Discover how expanding our back-office team helps founder Arlan Davine deliver tailored financial advice in Torquay.

Significant superannuation changes took effect on 1 July 2026. Find out how the new contribution caps and pension limits affect your wallet.

One year after starting Elevate Financial Planning, I reflect on the leap into business, the trust of my clients, and the gratitude I feel as a new financial year begins.

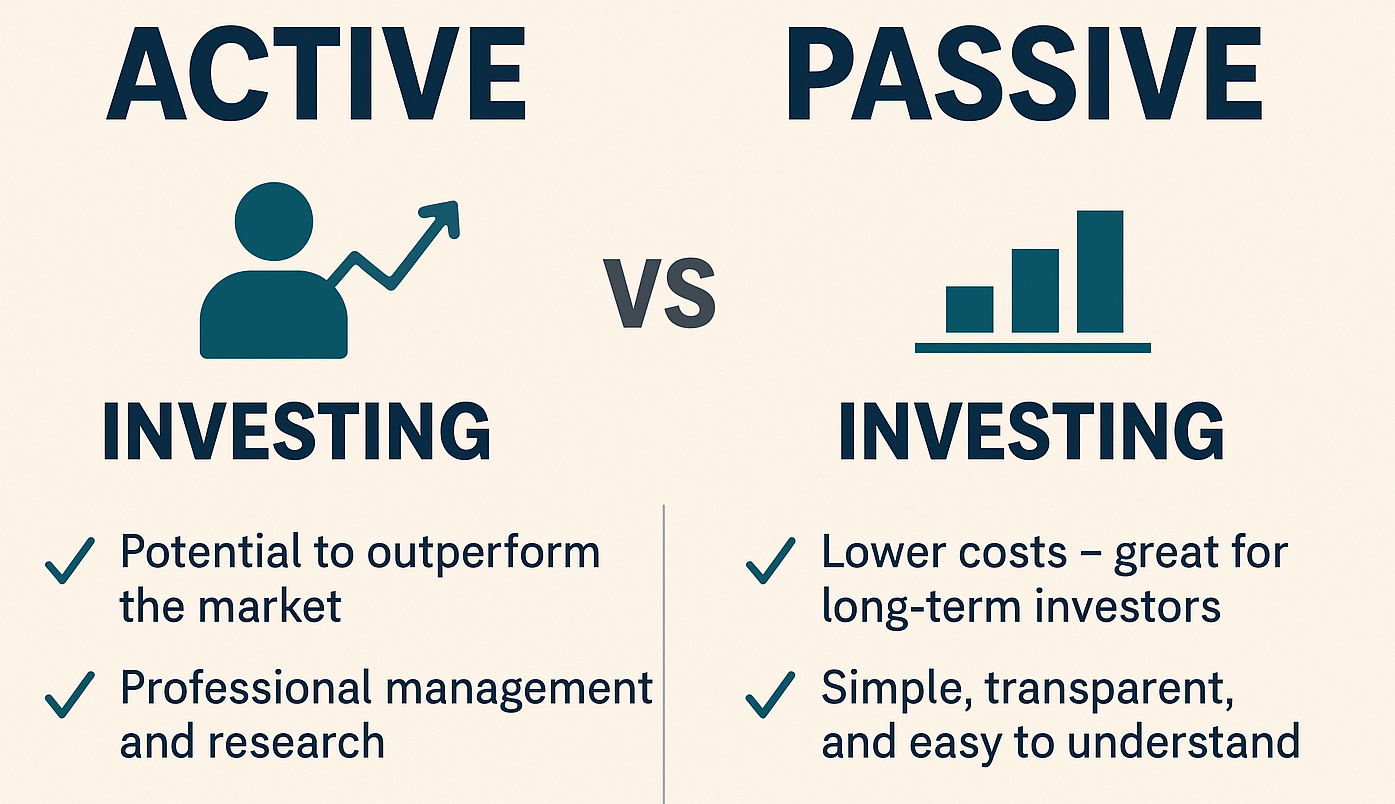

You don't need a fortune to build wealth—just time. Learn how micro-investing, regular habits, and compounding can supercharge your financial future.

From wills and insurance to super and emergency savings, discover the family financial checklist many Australians overlook — and how to protect what matters most.

Ready to boost your retirement savings? Discover 5 powerful ways to supercharge your super in 2026, including salary sacrificing, spouse contributions & more.

Feeling the pain at the pump from high petrol prices? Take back control. Discover 5 simple driving habits that can lower your fuel bill by up to 30%, starting today.

Growing up in Lake Bolac means community matters. When the Lake Bolac Kindergarten asked for toy donations, I was glad to give something small back to the town that shaped me.

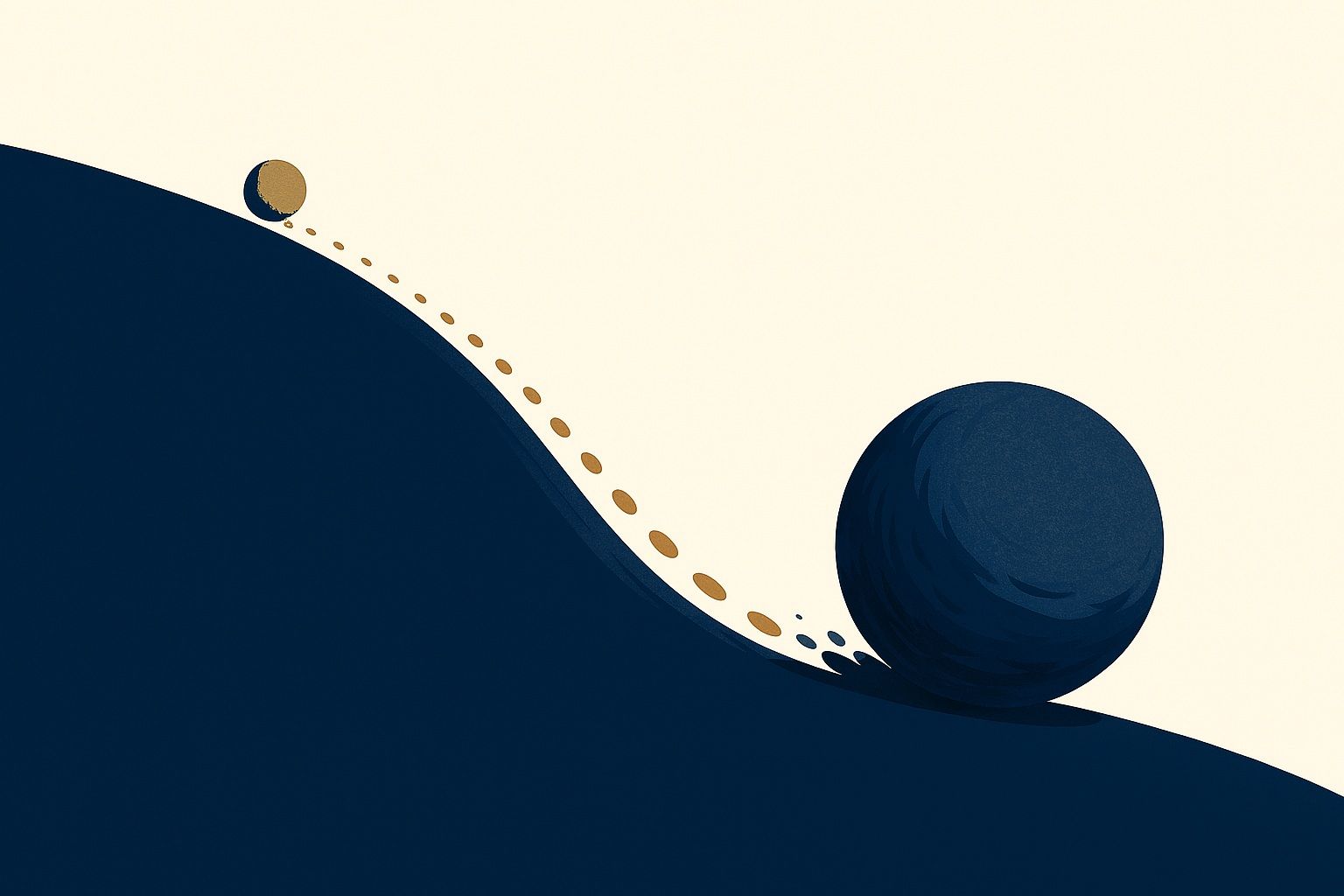

Discover how compounding can dramatically grow your superannuation. Learn the secret to building a large retirement nest egg, even with small contributions.

Successful in your career but not your finances? Even smart people fall into common traps. Learn the 5 biggest financial mistakes we see and how you can fix them.